Climate policy in Indonesia on analysis.

About This Series

Indonesia has ratified all the right climate agreement and has ambitious clean energy target. But in terms of its energy system, it remains to be going in the wrong direction.The idea for this series is: It’s not about intent, it’s about structure. The rules, contracts and institutions that govern Indonesia’s electricity sector are in fact set-up in such a way as to ensure fossil fuel interests are protected, irrespective of the target.Three articles. On the same topic, the three layers: 1) renewables do not fit this business model; 2) this ten year plan, coal expansion and green headlines; 3) in the region: why are all the others changing, but not Indonesia?

Renewable energy is not lacking in Indonesia. The renewable potential of the country is estimated to be around 3,692 GW (Tureah, 2025). Few countries in the world are as fortunate. Yet, year by year, Indonesia has been unable to make this potential into reality.

Despite the significant potential of renewable energy in Indonesia, the countries’ energy mix has not changed from 2020 to 2023, with only a slight increase from around 2% to 3% of renewables. This is well short of the government’s goal of 23% by 2025. Meanwhile, the electricity sector in Indonesia is still more carbon intensive than the electricity sector in China and India. Nonetheless, the mix of generation sources is approximately 60% from coal and 13% from renewables (Apriliyanti et al., 2024).

It’s easier said than done and people often talk about what is not the same as it was promised, in familiar terms. Some point to a lack of investment, insufficient grid or political will. All these are important, but they are at a surface level. The actual blocker is in the middle of the design of power sector in Indonesia.

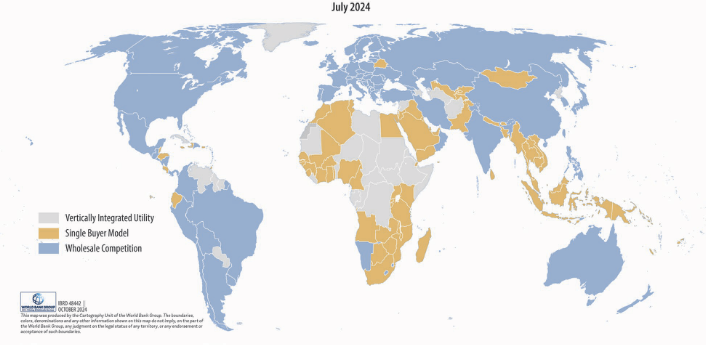

Source: (Ackura et al., 2024)

Indonesia is implementing Single Buyer Model (SBM) system (Ackura et al., 2024). Electricity can only be sold to most consumers as the state’s electricity company known as Perusahaan Listrik Negara (PLN). Independent power producers, such as renewable developers, must sell their power to PLN under long term power purchase agreements (PPAs) (Sastrawijaya et al., 2025). After that, PLN only resells the electricity to end users.

This is the structure that forms the foundation for all that ensues. It determines which projects are constructed, which projects are funded and which technologies are crowded out. And at the moment it’s not going in the same direction as the energy transition.

A system for the protection of coal.

PLN’s key task is to ensure that electricity is available and competitive for consumers. That’s a natural focus to have. But, in fact, the environmental and long-term climate costs and risks are not primary concerns. This, researchers have termed, is collective conservatism: the desire to foist the status quo on the minds of the entrenched interests of the utility and the much wider governance system that jeopardize loss of assets (Apriliyanti et al., 2024).

It is only natural that PLN has take-or-pay system in the PPA (Power Purchase Agreement) with the IPP that ensures IPP’s return on investment. Such contracts are ones in which PLN has to buy a specific amount of electricity from coal power producers, even if electricity demand is low. Penalties are paid regardless of whether PLN is able to take the electricity.

This is to ensure profitability of coal plants and place the risk on the public balance sheet. The same take-or-pay applies to fossil fuels power plants. The IEA estimates that under such contracts, the coal capacity in Java Bali alone will be about two-thirds of the expected peak demand in 2025 (Hart et al., 2025). This is due to the aging plants, higher maintenance costs and compliance requirements. Nevertheless, the PLN has to pay the coal IPPs as if they are generating according to their contract.

Unfortunately, it’s not just an inefficiency problem. This is obviously a failure of climate policy. The investments are still continuing to be made in fossil and the renewable projects can’t be sold.

This is not a common practice in Indonesia.

The power market structure is becoming more and more abnormal in the world including Indonesia. In 1989, and later, 158 countries or more have moved away from a fully-centralised and vertically integrated utility model (Ackura et al., 2024). Add multiple competition, independent system operator(s), or multiple buyers.

It’s simple: A normal open market and competitive market structure shows to us that it delivers better outcomes. They stimulate private investment, boost generation and accelerate deployment of renewables.

Apparently, however, in Indonesia, they still have a partial reform model. PLN is the only buyer and gatekeeper for private companies that want to construct power plants. The outcome is a system that has the worst of both worlds: the downsides of liberalization and the downsides of monopoly power.

Lessons from neighbors.

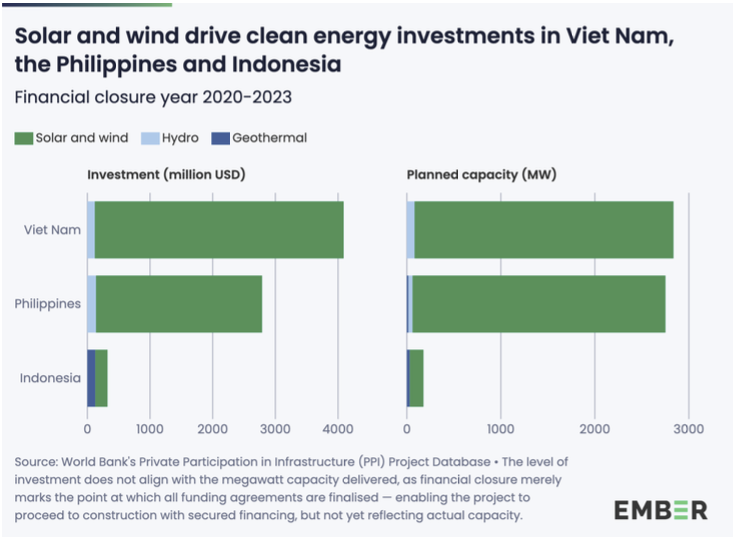

Vietnam is one neighbor country to be an example for Indonesia’s power sector. It was like Indonesia where there was a single state-owned utility (EVN). However, in March 2025, Vietnam rolled out a Direct Power Purchase Agreement framework via Decree 57. This will allow renewable generators to connect their generating facilities to the large consumers and sell the electricity generated by the renewable generators either physically or virtually through the national grid (Hau, 2025).

The effects may be great. The studies show that, for Vietnam, renewables could reach well above 40% if all the direct PPAs are fully implemented, especially with industrial consumers (Setyawati et al., 2025).

The Philippines went down a different path but ended up in a similar location. Renewable capacity is to be procured through Green Energy Auction Programme (GEAP) which is a competitive bidding process (Bunye & Evangelista, 2025). Importantly, there market reform is viewed as a component of climate compliance as opposed to being primarily an economic policy. This has enabled the country to access climate finance and international investment.

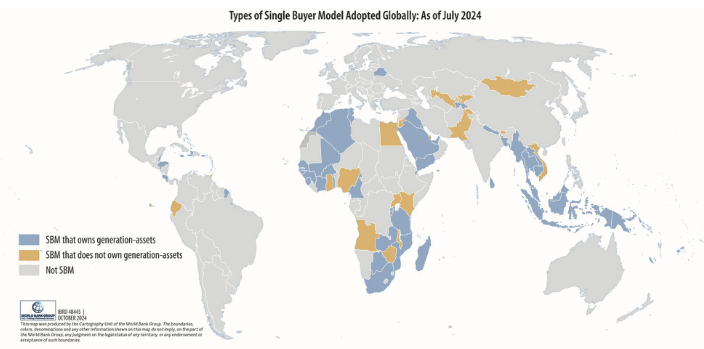

Source: (Setyawati et al., 2025)

Indonesia stands apart. There is significant regulatory barriers in the corporate sector for renewable procurement. There is no practical way for companies that want to buy clean electricity to do so.

There are three issues that continue to occur.

The corporate renewable market is suppressed in the first place in Indonesia. Corporate PPAs are a huge contributor to renewable growth around the world. They help businesses reach their emission targets, and can give developers certainty of revenue over the long-term. In the prevailing system in Indonesia, this is not allowed. PLN’s fight for equity shares in projects without risk involvement (e.g. financial risk in case of cost overrun, operational problems etc.) do not encourage private investment (Tureah, 2025). This behaviour results in an effect of discouraging private investment.

Of course, what we see is not as serious as this. Data centers, smelters and manufacturing facilities are growing at a rapid pace. By 2030, the estimated amount of domestic data center doubles the capacity (Yustika & Bachtiar, 2025). These sectors demand huge quantities of reliable and pollution-free power. If they don’t, then they’ll invest somewhere else.

Secondly the existing model exposes to stranded assets. Early plant retirement is cost intensive, due to coal PPAs being guarantees of payment. Whether or not they are required, it is safer to leave them on as it is cheaper, just in case. Studies indicate that in order for the Paris Agreement to be fulfilled, coal plants need to be phased out decades before they will be phased out anyway (von Dulong, 2023). In contrast, Indonesia is taking the opposite step in the form of the creation of new captive coal power for industries.

As industrial policy is now formulated, it may become a tomorrow’s “stranded asset problem”, especially as carbon border taxes and environmental regulations increase in export markets.

Thirdly, there is a significant disconnect in terms of governance of power supply. National climate goals are one thing, PLN’s planning is another. The proportion of coal to be be reduced to a cap of 30% by 2025. To be sure, more than 60% of PLN’s plans were made (Wiguna, 2025). The 2020 renewables target saw a large miss.

This is clearly not a coincidence. One government institution has all procurement and its internal priorities are national climate policy.

What is in reform that would actually mean to this sector in Indonesia.

The real reform must be started by Indonesia with the separation of duties. Transmission and system operation should not be dependent on generation and offtake (Ackura et al., 2024). This has to be the ground rule to have an independent and fair grid access. This has to be the ground rule to have an independent and fair grid access. This is what most countries that sped up renewables’ deployment did.

Further, Indonesia must formalise the direct PPA system. Opportunities for large consumers to buy renewable power directly from producers, with transparent rules on the basis of the grid. The Vietnamese model provides a good blueprint.

Last but not least, take or pay needs to be rethought. Coal contracts must be re-negotiated to stop renewables being blocked at dispatch (Munandar, 2026). There must be a transparent and open coal retirement timetable. This will include blended finance and international assistance, including JETP funds, to ensure the costs are kept down while not threatening the tariff and PLN’s balance sheet.

The choice ahead.

The climate goals of Indonesia are ambitious in many respects. Needless to say, Indonesia also needs to build structural reform as its base to realize this ambition. It will be gradual until the power sector shifts to a single buyer model that does not discriminate against renewables, and in favor of coal.

Other countries have shown that outcome is a function of market design. The greater the demand, the more the competition, the more the visibility on the grid, the faster the deployment of clean energy and lower the costs.

Indonesia is not lacking in resource. It’s not endowed with a principle of fair competition for those resources. That doesn’t mean it will end, however, as the country will continue to discuss energy transition while constructing a carbon-lock-in future.

Keywords: Single Buyer Model, Renewable Energy Potential, Coal Protection, Market Reform, PLN

References

Ackura, E., Adewole, A. O., & Mutambatsere, E. (2024). Repurposing Power Markets: The Path to Sustainable and Affordable Energy for All. https://www.ifc.org/content/dam/ifc/doc/2024/repurposing-power-makets.pdf

Apriliyanti, I. D., Nugraha, D. B., Kristiansen, S., & Overland, I. (2024). To reform or not reform? Competing energy transition perspectives on Indonesia’s monopoly electricity supplier Perusahaan Listrik Negara (PLN). Energy Research and Social Science, 118. https://doi.org/10.1016/j.erss.2024.103797

Bunye, P., & Evangelista, R. (2025, September 25). Renewable Energy 2025: Philipines Trends and Development. https://practiceguides.chambers.com/practice-guides/renewable-energy-2025/philippines/trends-and-developments

Hart, C., Lopez, L., & Warichet, J. (2025). Enhancing Indonesia’s Power System: Pathways to meet the renewables targets in 2025 and beyond. https://www.iea.org/reports/enhancing-indonesias-power-system

Hau, V. B. (2025, December 8). Grid upgrades and market reform: Reshaping Vietnam’s renewable energy market. https://www.reccessary.com/en/insight/grid-upgrades-and-market-reform-vietnam

Munandar, A. (2026, April 21). Indonesia talks energy transition, but why does coal still rule? https://moderndiplomacy.eu/2026/04/21/indonesia-

Sastrawijaya, K., Rustani, A. V., Hendrika, R., & Lazuardi M Hida. (2025, September 25). Renewable Energy 2025: Indonesia Trends and Developments. https://practiceguides.chambers.com/practice-guides/renewable-energy-2025/indonesia/trends-and-developments

Setyawati, D., Nadhila, S., & Demoral, A. (2025). From emission-intensive to investment hotspots: Championing renewables in 3 ASEAN economies. https://ember-energy.org/app/uploads/2025/12/Championing-renewables-in-3-ASEAN-economies-PDF.pdf

Tureah, G. (2025, February 6). The Country of Perpetual Potential: Indonesia’s Barriers in Renewable Energy Transition Gregy Tureah. Chicago Policy Review. https://chicagopolicyreview.org/2025/02/06/the-country-of-perpetual-potential-indonesias-barriers-in-renewable-energy-transition/

von Dulong, A. (2023). Concentration of asset owners exposed to power sector stranded assets may trigger climate policy resistance. Nature Communications, 14(1). https://doi.org/10.1038/s41467-023-42031-w

Wiguna, B. A. (2025, February 5). Indonesia’s energy transition needs a decentralised approach . https://doi.org/10.59425/eabc.1738792800

Yustika, M., & Bachtiar, R. (2025, December 24). After years at an energy crossroads, can Indonesia pivot in 2026? Key Findings. https://ieefa.org/resources/after-years-energy-crossroads-can-indonesia-pivot-2026

Mỗi tựa game giải trí tại danh mục đều do nhà phát hành đình đám hàng đầu thế giới liên kết với sân chơi đem đến. xn88 Điều này giúp đảm bảo mọi trò chơi đều thiết kế, cập nhật tính năng mới mẻ mỗi ngày giúp đáp ứng tất cả nhu cầu săn thưởng của anh em. Ngoài việc có cơ hội trải nghiệm tính năng mới mẻ thì anh em còn được khám phá tỷ lệ trả thưởng siêu cao cùng với quy trình thanh toán minh bạch, rõ ràng và an toàn tuyệt đối. TONY07-03