This is the third of a series of articles about the energy transition policy of Indonesia. The first article was regarding the issues of the RUPTL 2025-2034, which is the plan of the domestic climate commitments in Indonesia. In the last article, we discussed the issues regarding domestic climate commitments in Indonesia, which were in the RUPTL planning document for 2025-2034. This article is to focus on the export side.

At the State Opening of the Parliament held on May 20, 2006, President Prabowo Subianto made a promise to stop exports of coal, palm oil and ferroalloys via private companies. Those would instead go through one government-controlled company, PT Danantara Sumberdaya Indonesia (DSI). This new entity came into existence with the aim of rationalisation of the government. (Maliki Baskoro, 2026)

The issue to be solved is authentic. For decades, evasion of tax and royalty to the Government of Indonesia has resulted in under invoicing of commodity by producers, that is, the commodity export price to the destination in Singapore and Dubai is in artificial price. This is a perfectly valid grievance on the part of the government.

However, choosing a solution to accompany is not without sequelae outside of trade governance, nor will be the institution that will be established to implement this solution. From the RUPTL 2025-2034 mentioned in the last article, it can be seen that there is a direction of movement from the RUPTL from the previous article, namely in the direction of shifting from coal which is not under the control of the state of Indonesia. Acting directly and centrally to gain control of the coal economy, domestically and in the export sphere as well.

How DSI works

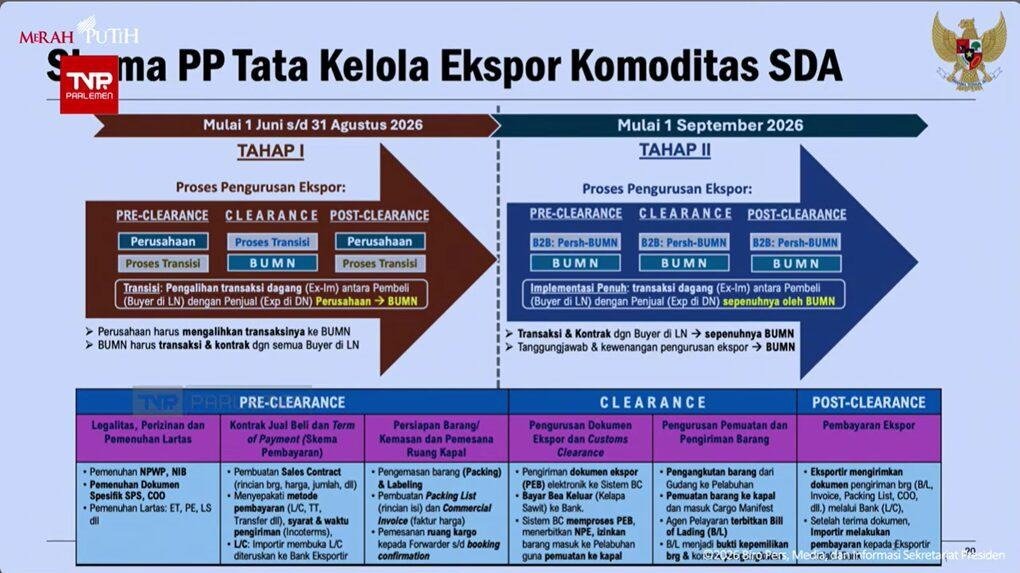

The architectural design is simple. The President issued the Government Regulation on the Government of Natural Resource Commodity Exports on 20 May 2026, which dictates that exports of palm oil, coal and ferroalloy are to be made by a state-owned enterprise as sole exporter. (Hegarty, 2026)

It’s going to be phased in. Before the export management policy by PT DSI is implemented, the government has determined a transition period for the export management for three months, starting from June 1, 2026 to August 31, 2026, and will be fully implemented throughout the country on January 1, 2027 (Harianto et al., 2026). Exporters report to DSI and continue to export as they would do under normal circumstances during transition period. From September 2026, the entire export chain (contracts, shipments, payments) is taken over by DSI.

Source: (Hegarty, 2026)

In addition the financial control level must be stated. As of June 1st, 2026, the 100% of export proceeds of natural resources of all export companies in Indonesia will be deposited in the Indonesian state-owned banks (Widianto et al., 2026). It’s a large administrative task. It merely transfers the revenue of coal exportation that is around USD 30-40 billion a year from the Off Shore Financial Centers to the banking area in Indonesia.

DSI will be facing tons of scaling. Indonesia is one of the biggest exporters of thermal coal in the world, having the export capacity of about 350-400 MT/year. (Putri & Putri, 2026)

The counter argument: Can we even achieve a phase out through DSI?

Others have made counter arguments. For this reason they say, “You can’t relax what you can’t see and can’t control.” In the earlier, decentralized system, there were thousands of individual coal producers and offshore traders were unable to coordinate supply-side cuts in practice. This puts a leverage in the hands of the government as DSI brings all this under one roof of the government: Volume reduction of exports, Benchmark pricing and Negotiate exit arrangements based on consolidated position with major buyers like India / China.

This is a valid argument which shouldn’t be discarded. In principle, managed phase-down needs a centralized management.

The issue is that this is not what DSI was meant to do, and the institutional is not geared up for.

Firstly, the Prabowo/Airlangga Hartarto/Danantara CEO Rosan Roeslani triumvirate will tackle the under-invoicing and revenue capture problem as outlined in the founding document of the DSI. Volume reduction targets, coal phase-down timelines and transition governance are not mentioned in any of the founding documents. There is a difference between the revenue transparency maximising institution and an institution to help manage revenue loss. Such a mandate would have to be re-worded.

Secondly, DSI is the sovereign wealth fund of Indonesia, Danantara, which was founded in February 2025 with the philosophy of “maximising the return of state assets. A lower volume of coal exports will adversely impact on a unit’s performance on the Danantara’s portfolio. If DSI is to be a phase-out solution, it would need to come off that ROA-thinking and that hasn’t been suggested.

Third, in the RUPTL 2025-2034, it’s vice versa. If DSI were to be used as a phase out tool – you would expect that, as export demand slows down, then DSI will become available for domestic demand. Instead, previous article in this series saw coal maintaining its share of electricity generation at 57% in 2030, a figure that is virtually unchanged from today. No policy synchronisation with the two policies. Same thing: more coal not less.

Centralization-as-phase-out is a policy that could be put in place as intended. Not a reference to the policy proclaimed.

The issue of Investor confidence.

The announcement by the DSI, though, lacks the much-needed clarity from both the regulatory and technical and operational parameters fronts, and is the next step in the sequence of policy measures to choke government’s hold on the coal sector that is gradually strangling investor confidence. The practice of issuing mining quotas for one year instead of three years, as was done in 2023, has already been resumed by the government. (Chaturverdi, 2026)

This is crucial not only to the coal industry. To achieve the backloaded clean energy targets in the RUPTL, Indonesia must lure big renewable energy investments. International capital allocators take into account not only energy-specific policies, but also the overall regulatory environment. If a government preaches a radical policy of export centralisation, involving almost no stakeholders, has almost all the key issues left unaddressed, and announces this policy within a few weeks, then a few things can be said about predictability and the rule of law – and renewables investors.

Foreign investors would not consider any additional centralisation as regulatory stability. In the longer term this can limit the investment potential, especially from multinational commodity companies. The logistics and costs involved with handling the vast quantities of commodities on export, managed by many thousands of companies, shipping arrangements, insurance contracts and international relationships is a very great challenge. (Translindo, 2026)

DSI’s registration took place just before the parliamentary speech made by Prabowo. It is never been used. There are still no answers on its fee structure, its reference pricing methodology or how it will deal with long-term contracts in place. Managed phase down is a much more challenging task of governance and can only be done by an institution that already provides managed basic export routing.

The agency has two policies and only one direction.

On the surface it may seem like a bad transition plan to have the renewable targets deferred to the 2030s in the RUPTL 2025-2034. But DSI, in isolation, could be seen as a much-needed overhaul of the revenue governance structure. However, they do combine to form another, more complete and more disturbing, image – a series of bricks that connect to each other.

It is as if Prabowo’s government is doing cement walling for Indonesia, whether in the domestic market of coal to be used in the national electricity system (RUPTL) or in the market of coal commodities (DSI) internationally. They are a similar policy mistakes. There is one common theme that unites them: the fiscal architecture in Indonesia continues to be structurally coal dependent and the government has opted to make things worse, not to start the hard task of unwinding it.

There is still so much to be done between the policy paper and realities. There is a lack of alignment between the national energy planning targets and NDC targets and the climate commitments seem unrealistic for Indonesia. Coal’s trajectory needs to turn down significantly in order to achieve the 2060 net zero goal set in the NDC (Cerah, 2025). The flow of the RUPTL and DSI is opposite each other.

The next key elements of believable climate governance.

There are three explicit changes that need to be done to make DSI a real climate instrument and not just a mechanism to capture revenues: It will have to include a mandate to decrease coal export volume, and specific and binding time frames. It would have to be apart from and separate to Danantara’s ROA logic. But its use should be synced with a new RUPTL (Reference Unit Power Target of Load) that would decrease the use of coal at home and the export of coal.

There aren’t any such situations. Until they are, DSI can best be thought of as the state gaining a tighter grip on an industry it doesn’t plan to let go of.

But climate credibility has nothing to do with the problem, as this is a matter of what Indonesia’s government says in international conferences. It’s what it is actually committed to doing in the next ten years in its plan for electricity, in its export governance and in its contracts for PPA that it says it is going to do. But, with respect thereto, the evidence, set forth in the foregoing articles of this series, is pretty clear that it points to a larger number of coal, more consolidated, more under the control of the State.

That is a choice. But it is not too late to do that, yet – and the window of opportunity to do so without incurring serious economic and climate damages is rapidly closing with every plan signed, every plant built, and every institution created on the basis that coal will continue to be the crucial part of the Indonesian economy well into the 2030s and beyond.

Keywords: Danantara Sumberdaya Indonesia, Investor Confidence, Centralized Export Control, Coal Governance, Revenue Capture

Reference.

Cerah, Y. I. (2025, October 27). NDC Indonesia: Concrete Climate Commitment or Empty Promise? Yayasan Indonesia Cerah. https://www.cerah.or.id/publications/article/detail/ndc-indonesia-concrete-climate-commitment-or-empty-promise

Chaturverdi, S. (2026, May 26). Indonesia’s coal policy shifts test investor confidence. https://www.argusmedia.com/en/news-and-insights/latest-market-news/2831354-indonesia-s-coal-policy-shifts-test-investor-confidence

Harianto, M., Sulistiyandari, R., & Rahman, R. (2026, May 29). Danantara Sumber Indonesia won’t profit from CPO export policy: Gov’t. Antara News. https://en.antaranews.com/news/417345/danantara-sumber-indonesia-wont-profit-from-cpo-export-policy-govt

Hegarty, K. (2026, May 21). Indonesia’s Commodity Export Plan: What We Know So Far. Palm Oil Monitor. https://palmoilmonitor.org/2026/05/21/indonesias-commodity-export-plan-what-we-know-so-far/

Maliki Baskoro, F. (2026, May 20). What We Know So Far About Danantara Sumberdaya, Indonesia’s New Export Entity. https://jakartaglobe.id/business/what-we-know-so-far-about-danantara-sumberdaya-indonesias-new-export-entity

Putri, N. C., & Putri, A. (2026, May 26). Indonesia sets September 2026 rollout for centralized commodity export system. Indonesia Business Post. https://indonesiabusinesspost.com/6666/policy/indonesia-sets-september-2026-rollout-for-centralized-commodity-export-system

Translindo. (2026). Prabowo Establishes State-Owned Export Company, PT Danantara Sumber Daya Indonesia. https://www.translindogroup.com/2026/05/22/prabowo-establishes-state-owned-export-company-pt-danantara-sumber-daya-indonesia/

Widianto, S., Suroyo, G., & Nangoy, F. (2026, May 20). Indonesia to bring commodity exports under centralised control, president says. Reuters. https://www.investing.com/news/economy-news/indonesia-to-bring-commodity-exports-under-centralised-control-president-says-4700776

XN88 có tính năng “tự khóa tài khoản” – hỗ trợ người chơi muốn tạm nghỉ hoặc kiểm soát hành vi cá cược. TONY07-03

XN88 có tính năng “tự khóa tài khoản” – hỗ trợ người chơi muốn tạm nghỉ hoặc kiểm soát hành vi cá cược. TONY07-03