Imagine living in a country where government pays your 95% electricity bill because of oil abundance. Yet, behind this illusion lies a hidden crisis that forcing Kuwait to beg the desert sun before the global oil market leaves them behind.

Gulf countries like Kuwait are likely to be the last to exit the fossil fuel market, as they are among the world’s cheapest producers. It is interesting to know Kuwait, a small-rich state in the MENA region is one of the largest oil producers globally, holding a 3% share of total world production with an output of 2.91 million barrels per day. As a rentier state, Kuwait faces persistent institutional inefficiencies, a lack of democratic governance, and low public pressure. In 2021, a study shows oil and natural gas revenues accounted for 57% of government income, while petroleum exports contributed 78% of total export earnings. Due to its limited agricultural condition, Kuwait’s desert-dominated landscape and vast hinterlands offer strong solar and wind energy potential, making it suited to support energy diversification efforts.

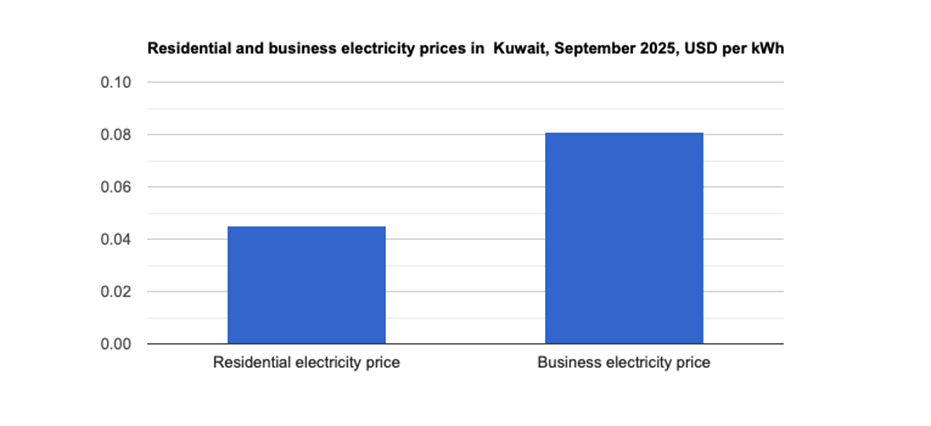

Kuwait’s dependency on oil exports has derives a large portion of its revenue from the export of natural resources rather than regional taxation to. This is a challenge to prioritize which agenda comes first, transition away or phasedown fossil fuel. Furthermore, Kuwait’s electricity is generously subsidized by the government up to 95%, resulting a low-electricity prices (0,046 USD/kWh) for residents, produced from oil of 99.77%, wind 0.03%, and solar 0.20%. These conditions create dilemma: Kuwait must balance its fiscal reliance on fossil fuels with the commitment toward clean energy.

Source: Ministry of Electricity, Water, and Renewable Energy

This article investigates both the challenges and opportunity in Kuwait’s energy transition. It focuses on the political tensions that have slowed down progress toward clean energy targets, as well as the potential of Kuwait’s renewable energy market will be, and addresses the following questions: (1) How do Kuwait’s political structures and main challenges that influence the clean energy transition?, (2) What are the opportunities for scaling up renewable energy in a heavily reliant on fossil fuel exports country?

Based on Kuwait Energy Outlook 2023, the country is dominated by dirty energies that is dominating African and Asian markets as exporter, the highest per capita energy consumers (contributing 40.5% GDP[1]), and CO2 emitters. Yet, rising global pressure to decarbonize and oil price volatility (pricing up around $90–110 per barrel since the late 2000s) have exposed the long-term risks of this dependence. The financing of energy projects still heavily relies on government funding, making it difficult for the private sector to participate, resulting in low involvement in renewable energy projects. This poses a significant challenge to energy diversification, as the existing infrastructure is predominantly designed for fossil fuels rather than clean energy. While the government has plans to develop alternative energy sources, solar and wind energy infrastructure remains in its early stages. Despite the country’s abundant sunlight, its utilization capacity is still far from optimal. This is largely due to a lack of capacity in generation capacity. This is largely due to a lack of capacity in generation capacity. Recent study in 2017 shows the daily minimum and maximum consumption of energy in 2017 are 99,546 MWh and 108,438 MWh with total Kuwait power generation capacity 19,913MWh, which demand exceeds the country’s power capacity. This indicates that the energy sector is not yet fully prepared to handle demand spikes, especially during the summer when residents rely heavily on air-conditioning.

Despite these signals, Kuwait’s energy sector still remains dominated by few state institutions such as the Kuwait Petroleum Corporation (KPC), Kuwait National Petroleum Company (KNPC), and the Ministry of Electricity, Water and Renewable Energy (MEWRE). Government offices dominate and manage most of the energy sector in Kuwait. This setup makes the industry highly sensitive to political changes. Frequent political shifts often slow down energy projects, fragmented regulations and a non-mature large-scale system are the main barriers and unpredictable. Events like replacing cabinet members or closing parliament create an unstable environment. Foreign investors price at risk, and renewable energy programmes tend to suffer most, given their longer development timelines and greater sensitivity to shifts in the regulatory environment.

This happens because of political disputes and shifting rules. A clear example is the canceled Al-Dibdibah solar project in 2020, when it supposed to start operating in 2021. Officials stopped this plan because of the global pandemic and its negative impact on oil and financial markets. Furthermore, Kuwait does not have one independent office to oversee its energy rules. The task of making rules is spread across several different groups instead. This shared power leads to confusion, slow responses, and repeating the same work to a vicious circle that never ends. The government tried to improve teamwork between public offices and private companies in 2008 by creating the Kuwait Authority for Partnership Projects. However, this program has seen very little success over the years. But if we looked data from 2021, modern renewables made up just 0.07% of final energy consumption, underscoring inefficiency and policy enforcement. Moreover, the country is far from meeting its BAU (business-as-usual) target of a 7.4% emission reduction by 2035, even as projections suggest global oil demand may decline by up to 40% by 2040. Kuwait needs policies that focused on accelerating securing investment and deployment of renewable energy.

Amid the challenges it faces, Kuwait actually possesses several strategic opportunities that can be leveraged in the regional context and in the potential export of clean energy. While Kuwait does not rely on importing electricity, it holds significant potential to export energy to neighboring countries such as Oman (which has a target of 20% renewable electricity), Saudi Arabia at 50%, and the UAE at 44% by 2030, and potentially even to Iraq. The main issue is that Kuwait lacks interconnection with neighboring countries. There are significant erratic nature limitations and its power grid remains relatively isolated and highly vulnerable to climate disasters. This isolation restricts Kuwait’s flexibility in managing cross-border energy supply and demand. However, with substantial investment in cross-border interconnection infrastructure, such as a Shagaya Renewable Energy Park (SREP) which produces electricity via PV, wind, and solar power and estimated will be completed in 2027. It is potential to connect national to inter-regional energy market in the Gulf and increase state revenue not only from dirty energies.

On the other hand, electricity financing in Kuwait has long relied on government subsidies, which reduces the economic incentive for households to invest in renewable energy. As an alternative, the government could consider implementing a Feed-in-Tariff (FIT) policy scheme. Recent study has shown that FIT is the most viable investment model for PV systems, particularly because Kuwait is predominantly composed of residential areas, making it well-suited for rooftop solar adoption. The study reported a Net Present Value (NPV) of $32,885, an Internal Rate of Return (IRR) of 14.9%, and an estimated annual revenue of $685.50, which means allowing payback in around 7 years. By asking residents to pay for their electricity through a Feed in Tariff (FIT) plan can create reliable investment chances.

This change would also lower government spending over the years. The new clean energy auction rules support this direction as well. These recent rules suggest that the green power market in Kuwait is starting to become stable. For instance, the Shagaya Phase II project opened in 2024 for 1.1 GW of solar PV capacity through a transparent auction mechanism under the Kuwait Authority for Partnership Projects (KAPP), with a 30-year power purchase agreement (PPA) structure and scheduled completion by 2027. Kuwait’s auction model has also succeeded in attracting globally recognized developers such as ACWA Power, Masdar, EDF, TotalEnergies, and Jinko Power. Moreover, the average electricity price in Kuwait has increased from $26.88 MWh in 2022 to $27.11 MWh in 2023. It is clearly demonstrating trust in the country’s evolving regulatory and RE price reforms. The market may strengthen in the future with PPP intervention, as time goes by.

What we can learn at the end, Kuwait’s commitment to renewable is still not strong enough to replace oil and gas in its economy or energy mix. It can be seen from few policy reforms, mostly been small and limited. Although there has been some progress, such as renewable energy auctions and large-scale plans like the Shagaya project, Kuwait still relies heavily on fossil fuels for both national revenue and electricity generation. Government subsidies for electricity and a lack of incentives for private and household investment have slowed down the clean energy transition.

Keywords: Kuwait energy transition, solar power, energy subsidies

+ There are no comments

Add yours